Principal Component Analysis (PCA)

PCA is the most widely used dimensionality reduction technique. It transforms data into a new coordinate system where the axes (principal components) capture maximum variance.

The Core Idea

Find directions (principal components) that:

- Capture maximum variance in the data

- Are orthogonal (perpendicular) to each other

- Are ordered by variance explained

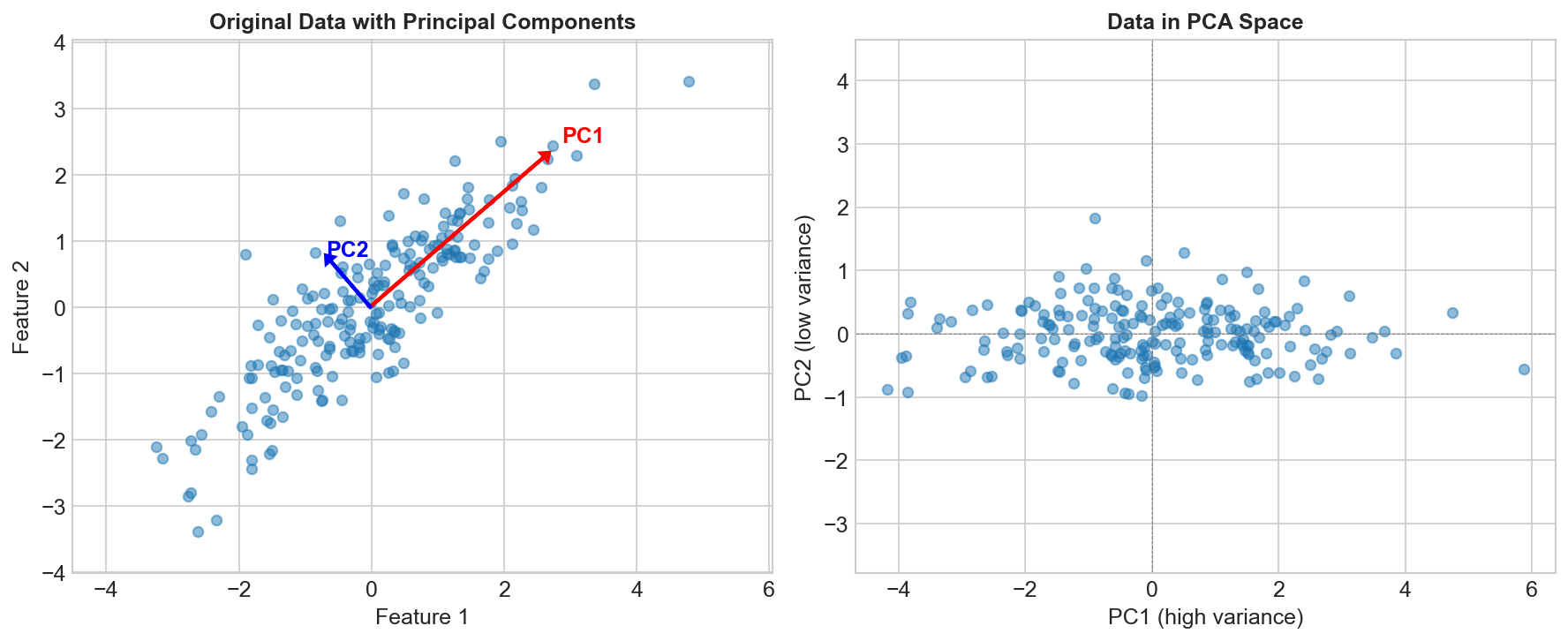

Original 2D data: After PCA:

• • PC1 →

• • • • • • •

• • • • • • •

• • • ↑

• • PC2

The Algorithm

Step 1: Center the Data

X_centered = X - mean(X)

Step 2: Compute Covariance Matrix

Σ = (1/n) × Xᵀ × X

Step 3: Find Eigenvectors and Eigenvalues

Σv = λv

Eigenvectors = principal component directions

Eigenvalues = variance explained by each component

Step 4: Sort and Select

Sort eigenvectors by eigenvalue (descending)

Keep top k components

Step 5: Transform

X_reduced = X_centered × W

Where W = [v₁, v₂, ..., vₖ] (top k eigenvectors)

Variance Explained

Individual Component

Variance explained by PCᵢ = λᵢ / Σλⱼ

Cumulative Variance

Cumulative = Σᵢ₌₁ᵏ λᵢ / Σλⱼ

Often keep components that explain 95% of variance.

Choosing Number of Components

Scree Plot

Plot eigenvalues, look for "elbow":

Variance

|\

| \

| \__

| \___

|_________

PC

Cumulative Variance Threshold

pca = PCA(n_components=0.95) # Keep 95% of variance

Kaiser Criterion

Keep components with eigenvalue > 1 (when using correlation matrix).

PCA Properties

What PCA Does

- Decorrelates features

- Orders by importance (variance)

- Reduces dimensionality

- Can reveal hidden structure

What PCA Doesn't Do

- Consider class labels (unsupervised)

- Guarantee better classification

- Handle non-linear relationships

- Work well with categorical data

When to Use PCA

Good for:

- Visualization (reduce to 2-3 dimensions)

- Noise reduction (remove low-variance components)

- Feature decorrelation

- Speeding up other algorithms

- Handling multicollinearity

Not good for:

- When all features are important

- Non-linear relationships (use kernel PCA)

- When interpretability is crucial

- Sparse data (use TruncatedSVD)

Practical Considerations

Scaling

from sklearn.preprocessing import StandardScaler

# ALWAYS scale before PCA!

X_scaled = StandardScaler().fit_transform(X)

pca.fit(X_scaled)

PCA is sensitive to scale. Standardize first!

Interpreting Components

# Component loadings (how much each feature contributes)

components = pca.components_ # Shape: (n_components, n_features)

# PC1 = 0.5*feature1 + 0.3*feature2 - 0.4*feature3 + ...

Reconstruction

# Transform to lower dimension

X_reduced = pca.transform(X_scaled)

# Reconstruct (with some loss)

X_reconstructed = pca.inverse_transform(X_reduced)

# Reconstruction error

error = np.mean((X_scaled - X_reconstructed)**2)

Code Example

from sklearn.decomposition import PCA

from sklearn.preprocessing import StandardScaler

import matplotlib.pyplot as plt

# Scale data

scaler = StandardScaler()

X_scaled = scaler.fit_transform(X)

# Fit PCA

pca = PCA(n_components=0.95) # Keep 95% variance

X_reduced = pca.fit_transform(X_scaled)

print(f"Original dimensions: {X.shape[1]}")

print(f"Reduced dimensions: {X_reduced.shape[1]}")

print(f"Variance explained: {pca.explained_variance_ratio_}")

# Plot cumulative variance

plt.plot(np.cumsum(pca.explained_variance_ratio_))

plt.xlabel('Number of Components')

plt.ylabel('Cumulative Variance Explained')

PCA vs Other Methods

| Method | Linear | Supervised | Use Case |

|---|---|---|---|

| PCA | Yes | No | General dim reduction |

| LDA | Yes | Yes | Classification |

| t-SNE | No | No | Visualization |

| UMAP | No | No | Visualization + structure |

| Autoencoders | No | No | Complex patterns |

Kernel PCA

For non-linear relationships:

from sklearn.decomposition import KernelPCA

kpca = KernelPCA(n_components=2, kernel='rbf')

X_kpca = kpca.fit_transform(X)

Maps to higher dimension, then applies PCA.

Key Takeaways

- PCA finds orthogonal directions of maximum variance

- Principal components are eigenvectors of covariance matrix

- Always standardize features before PCA

- Keep enough components to explain ~95% variance

- Good for visualization, denoising, and preprocessing

- Use kernel PCA for non-linear patterns